By Michael Roberts *

Bank stock prices have stabilized at the start of last week. And all the key officials at the Federal Reserve, the US Treasury and the European Central Bank are reassuring investors that the crisis is over. Last week, Fed Chair Jerome Powell called the U.S. banking system “strong and resilient” and there was no risk of a banking meltdown as in 2008-9. US treasury secretary Janet Yellen said that the US banking sector was “stabilizing”. The US banking system was strong. Over the pond, ECB president Lagarde has repeatedly told investors and analysts that there was “no trade-off” between fighting inflation by raising interest rates and preserving financial stability.

So all is well, or at least soon will be, given the massive liquidity support that the Fed and other US government lending bodies are offering. Also the stronger banks have stepped in to buy up the collapsing banks (SVB or Credit Suisse) or plough cash into failing ones (First Republic).

So is it all over? Well, it ain’t over til it’s over. The latest Fed data show that US banks lost $100bn in deposits in one week. Since the crisis started three weeks ago, while the large US banks have added $67bn, the small banks have lost $120bn and foreign-owned banks $45bn.

To cover these outflows and to prepare for more, US banks have borrowed $475bn from the Fed; split evenly between large and small banks, although relative to their size, small banks borrowed twice as much as the large ones.

The weakest banks in the US have been losing deposits for over two years to the stronger banks, but $500 billion has been withdrawn since the collapse of SVB on 10 March and $600bn since the Fed started raising interest rates. That’s a record.

Where are all these deposits going? Half of the $500bn in the last three weeks has gone into the bigger, stronger banks and half into money market funds. What is happening is that depositors (mainly rich individuals and small companies) are panicking that their bank might go bust like SVB and so are switching to ‘safer’ big banks. And also depositors see that, with rising interest rates across the board driven by central banks raising rates to ‘fight inflation’, there are better savings rates to be found in money market funds.

What are money market funds? These are not banks but financial institutions that offer a better rate than banks. How do they do this? They offer no banking services at all; MMFs are just investment vehicles that pay higher rates on cash. They can do this by in turn buying very short-term bonds like Treasury bills that offer just a slightly higher rate of return. Thus, the MMFs make a small interest gain but with huge amounts. More than $286bn has flooded into money market funds so far in March, making it the biggest month of inflows since the depths of the Covid-19 crisis. While that is not a massive shift relative to the size of the US banking system (it is less than 2% of the $17.5tn of bank deposits) it shows that nerves remain on edge.

And let’s remind ourselves how this all started. It started out with Silicon Valley Bank (SVB) closing its doors. Then the cryptocurrency Signature Bank. Then another bank First Republic had to be bailed out by a batch of large banks. Then over in Europe, Credit Suisse bank collapsed in less than 48 hours.

The immediate cause of these recent bank failures, as always, was a loss of liquidity. What do we mean by that? Depositors at the SVB, First Republic and Signature started to withdraw their cash big time, and these banks did not have the liquid cash to meet depositor demands.

Why was that? Two key reasons. First, much of the cash that had been deposited at these banks had been reinvested in assets by the bank boards that have hugely lost value in the last year or so. Second, many of the depositors at these banks, mainly small companies, had found that they were no longer making profits or getting extra funding from investors, but they still needed to pay their bills and staff. So, they started withdrawing cash rather than building it up.

Why did the assets of the banks lose value? It comes down to the rise in interest rates across the board in the financial sector, driven up by the actions of the Federal Reserve to raise its basic policy rate sharply and quickly supposedly to control inflation. How does that work?

Well, to make money, say banks offer depositors 2% a year interest on their deposits. They must cover that interest, either by making loans at a higher rate to customers, or by investing the depositors’ cash in other assets that earn a higher rate of interest. Banks can get that higher rate if they purchase financial assets that pay more interest or that they could sell at a profit (but might be riskier), like corporate, mortgage bonds, or stocks.

Banks can buy bonds, which are safer because banks get their money back in full at the end of maturity of the bond – say five years. And each year the bank receives a higher fixed rate of interest than the 2% its depositors are getting. It gets a higher rate because it cannot have its money back instantly but must wait, even for years.

The safest bonds to buy are government bonds because Uncle Sam is (probably) not going to default on redeeming the bond after five years. So SVB managers thought they were being very prudent by purchasing government bonds. But here is the problem.

If you buy a government bond for $1000 that “matures” in five years (i.e., you get your investment back in full in five years), which pays interest at, say, 4% a year, then if your deposit customers get only 2% a year, you are making money. But if the Federal Reserve hikes its policy rate by 1%, the banks must also raise their deposit rates accordingly or lose customers. The bank’s profit is reduced. But worse, the price of your existing £1000 bond in the secondary bond market (which is like a second-hand car market) falls. Why? Because, although your government bond still pays 4% every year, the differential between your bond interest and the going interest for cash or other short-term assets has narrowed.

Now if you need to sell your bond in the secondary market to get cash, any potential purchaser of your bond will not be willing to pay $1000 for it but say only $900. That’s because the purchaser, by paying only $900 and still getting the 4%, can now get an interest yield of 4/900 or 4.4%, making it more worthwhile to buy. SVB had a load of bonds that it bought “at par” ($1000) but worth less in the secondary market ($900). So it had “unrealized losses” on its books.

But why does that matter if it does not have to sell them? SVB could wait until the bonds mature, and then it gets all its investment money back plus interest over five years. But here is the second part of the problem for SVB. With the Fed hiking rates and the economy slowing down towards recession, particularly in the start-up tech sector in which SVB specialized, its customers were losing profits and so were forced to burn more cash and run down their deposits at SVB.

Eventually, SVB did not have enough liquid cash to meet withdrawals; instead, it had a lot of bonds that had not matured. When this became obvious to depositors, those that were not covered by state deposit insurance (anything over $250,000) panicked and there was a run on the bank. This became obvious when SVB announced that it would have to sell much of its bond holdings at a loss to cover withdrawals. The losses appeared to be so great that nobody would put new money into the bank and SVB declared bankruptcy.

So a lack of liquidity turned into insolvency – as it always does. How many small businesses find that if only they had got a little more from their bank or an investor, they could have ridden out a shortage of liquidity to stay in business? Instead, if they get no further help, they must fold. That is basically what happened at these banks.

But the argument goes that these are one-offs and the monetary authorities have acted quickly to stabilize the situation and stop depositor panic. There are two things that the government, the Fed, and the large banks have done. First, they have offered funds in order to meet depositors demand for their cash. Although in the US, any cash deposits over $250,000 are not covered by the government, the government has waived that threshold and said that it will cover all deposits (for these banks only) as an emergency measure.

Second, the Fed has set up a special lending instrument called the Bank Term Funding Program where banks can obtain loans for one year, using the bonds as collateral at par to get cash to meet depositor withdrawals. So, they don’t have to sell their bonds below par. These measures are aimed at stopping the “panic” run on banks.

But here is the rub. Some argue that SVB and the other banks are small fry and rather specialist. So they do not reflect wider systemic problems. But that is to be doubted. First, SVB was not a small bank, even it specialized in the tech sector – it was the 16th largest in the US and its downfall was the second biggest in US financial history. Moreover, a recent Federal Deposit Insurance Corporation report shows that SVB is not alone in have huge “unrealized losses” on its books. The total for all banks is currently $620 billion, or 2.7% of US GDP. That’s the potential hit to the banks or the economy if these losses are realized.

Indeed, 10% of banks have larger unrecognized losses than those at SVB. Nor was SVB the worst capitalized bank, with 10% of banks having lower capitalization than SVB. A recent study found that the banking system’s market value of assets is $2 trillion lower than suggested by their book value of assets (accounting for loan portfolios held to maturity). Marked-to-market bank assets have declined by an average of 10% across all the banks, with the bottom 5th percentile experiencing a decline of 20%. Worse, if the Fed continues to raise interest rates, bond prices will fall further, and the unrealized losses will increase, and more banks will face a lack of liquidity.

So, the current emergency measures may well not be enough. The current claim is that extra liquidity can be financed by larger and stronger banks taking over the weak and restoring financial stability with no hit to working people. This is the market solution where the big vultures cannibalize the dead carrion – for example, the UK’s SVB arm has been bought by HSBC for £1. In the case of Credit Suisse, the Swiss authorities forced a takeover by the larger UBS bank for a price one-fifth of CS’s current market value.

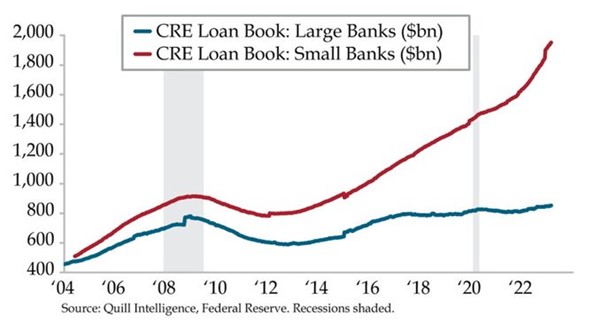

And that is not the end of the coming problems. US banks are heavily into commercial real estate (CRE) assets ie offices, plants, supermarket malls etc. When interest rates were very low or even near zero before the pandemic, small banks loaded up on real estate development lending and CRE bonds issued by developers. Borrowing as a share of bank reserves accelerated from 25% a year to 95% a year in early 2023 in small banks and 35% for big banks.

But commercial premises prices have been diving since the end of the pandemic, with many standing empty earning no rents. And now with commercial mortgage rates rising from the Fed and ECB hikes, many banks face the possibility of more defaults on their loans. Already in the last two weeks $3bn of loans have defaulted as developers collapse. In February, the largest office owner in Los Angeles, Brookfield, defaulted on $784m; in March Pacific Investment Co. defaulted on $1.7bn of mortgage notes and Blackstone defaulted on $562m bonds. And there are $270bn more of these CRE loans due for repayment. Moreover, these CRE loans are highly concentrated. Small banks hold 80% of total CRE loans worth $2.3trn.

The CRE loan risk is yet to hit. But it will hit the regional banks, already reeling, the hardest. And it’s a vicious spiral. CRE defaults hurt regional banks as falling office occupancy and rising interest rates depress property valuations, creating losses. In turn, regional banks hurt the real estate developers as they impose stricter lending standards post-SVB. This deprives commercial property borrowers of reasonably priced credit, crimping their profit margins and pushing up defaults.

And the other risk not yet resolved is international. The liquidation of the 167-year old Swiss international bank, Credit Suisse, and its forced takeover by its rival UBS was only made possible by writing off the $18bn value of all the CS secondary bonds held by hedge funds, private investors and other banks globally. Writing off bonds (debt) and saving the CS shareholders instead is unprecedented in financial law. That has raised the risk of holding such bank bonds, despite the assurances of the ECB that this would not happen in the Eurozone. As a result, investors have started to worry about other banks. In particular, their eyes have focused on the travails of Germany’s largest bank, Deutsche Bank, which after the events of Credit Suisse, is no longer too big to fail.

What that shows is that ECB president Lagarde’s repeated claim is nonsense that there is no ‘trade-off’ between fighting inflation with interest rate hikes and financial stability, as banks struggle to keep depositors and avoid defaults on loans. Indeed, a new paper by leading financial academics including the former governor of the Reserve Bank of India, finds that “the evidence suggests that the expansion and shrinkage of central bank balance sheets involves tradeoffs between monetary policy and financial stability.”

The dismissal of the dangers past and ahead by the monetary authorities should be no surprise to readers of this blog. Mainstream economist, Jason Furman, has noted that after the global financial crash of 2008-9, the Fed started doing regular Financial Stability Reports. But as Furman remarks: “The Fed completely missed what happened–not a hint of concern. One interpretation: incompetence. Another interpretation: this stuff is hard even if obvious in retrospect.” For example, the last November 2022, the FSR “generally presented a comforting picture of the financial sector. And it was especially serene about banks–both their capital and proneness to runs”.

The Fed’s FSR never stress-tested high interest rates. And yet when interest rates started to rise it should have been clear that banks had mark-to-market losses they were not accounting for in their hold to maturity portfolios. This risk was dismissed in in a footnote because the Fed thought that higher interest rates would mean gains for banks in net interest income. It was the same story with the Swiss National Bank and its confident assessment of Credit Suisse’s future just a few months ago.

As for regulation, I have beat the drum on the total failure of bank regulation to avoid crises on every occasion. As one bank legal expert put it: “In the wake of the 2008 crisis, Congress erected an enormous legal edifice to govern financial institutions–the Dodd-Frank Act. And we saw in the course of a weekend that it was all an expensive and wasteful Potemkin village. What good does it do to have a massive set of regulations…if they aren’t enforced? To have deposit insurance limits…if they are disregarded? Dodd-Frank is still on the books, but its prudential provisions are as good as dead. Why should anyone follow its requirements now, given that they’ll be disregarded as soon as they’re inconvenient? And why should the public have any confidence that they are protected if the rules aren’t followed? Indeed, did anyone even look at SVB’s resolution plan or was it all a show?”

“I really don’t know how one can teach prudential banking regulation after SVB. How can you teach the students the formal rules—supervision, exposure and concentration limits, prompt corrective action, deposit insurance caps—when you know that the rules aren’t followed?”

“The rules always get tossed out the window in financial crises and then there’s a lot of finger wagging and new rules that are followed until the next crisis, when they aren’t.”

And the head of the world’s top financial regulator, Pablo Hernández de Cos, chair of the Basel Committee on Banking Supervision, said last week “The only way to entirely prevent a bank run would be to require them to keep all of their deposits in highly liquid assets, but then you wouldn’t have banks any more”. What he means is that you would not have any banks that aim to make profits and speculate; but you could still have non-profit banks providing a public service. But, of course, that’s not on the agenda.

It now seems that the bust Silicon Valley Bank paid out huge bonuses to its senior executives based on the profitability of the bank – as a result, the executives invested in riskier long-term assets to boost profitability and so gain larger bonuses. And that’s not all. Just before the bank went bust, it made huge loans at favourable rates to senior officers, management and shareholders to the tune of $219m. Nice if you can get it – as an ‘insider’.

What went wrong at SVB? Fed chair Jay Powell put it this way: “At a basic level, Silicon Valley Bank management failed badly. They grew the bank very quickly. They exposed the bank to significant liquidity risk and interest rate risk. Didn’t hedge that risk.” But “we now know that supervisors saw these risks and intervened.” Really? If so, they were a bit late! “We know that SVB experienced an unprecedentedly rapid and massive bank run. This is a very large group of connected depositors, concentrated group of connected depositors in a very, very fast run. Faster than historical record would suggest.” So the Fed was caught out.

But don’t worry it won’t happen again. “For our part, we’re doing a review of supervision and regulation. My only interest is that we identify what went wrong here. How did this happen is the question. What went wrong. Try to find that. We will find that. And then make an assessment of what are the right policies to put in place so it doesn’t happen again. Then implement those policies.”

But this is a superficial explanation. Every time, there will be some fault-line in banking. As Marx explained, capitalism is a money or monetary economy. Production is not for direct consumption at the point of use. Production of commodities is for sale on a market to be exchanged for money. And money is necessary to purchase commodities.

Money and commodities are not the same thing, so the circulation of money and commodities is inherently subject to breakdown. At any time, the holders of cash may not decide to purchase commodities at going prices and instead hoard it. Then those selling commodities must cut prices or even go bust. Many things can trigger this breakdown in the exchange of money and commodities, or in money for financial assets like bonds or stocks – fictitious capital, Marx called it. And it can happen suddenly.

But the main underlying cause will be the overaccumulation of capital in the productive sectors of the economy or, in other words, falling profitability of investment and production. The tech companies’ customers at SVB had begun to lose profits and were suffering a loss of funding from so-called venture capitalists (investors in start-ups) because the investors could see profits falling. So that’s why the techs had to run down their cash deposits. This destroyed SVB’s liquidity and forced it to announce a fire sale of its bond assets. Alongside that interest rates rose increasing the cost of borrowing. This ‘liquidity’ crisis is now brewing in the real estate sector and in banks with large bond debts.

So the banking crisis is not over yet. Indeed, some argue that there could a rolling crisis that lasts for years — echoing what happened during the US [1980-90s savings and loan] crisis.

What is certain is that credit terms are tightening, bank lending will drop and companies in the productive sectors will find it increasingly difficult to raise funds to invest and households to buy big ticket items. That is going to accelerate economies into a slump this year. The bold optimism expressed before March that recession will be avoided will prove to be unfounded. Only last week, the Federal Reserve’s own forecasts for US economic growth this year were lowered to just 0.4%, which if met would mean at least two quarters of contraction in the middle of this year.

And if the current banking crisis becomes systemic, as it did in 2008, there will have to be ‘socialization’ of the losses suffered by the banking elite through government bailouts, driving up public sector debts (already at record highs); all to be serviced at the expense of the rest of us through increased taxation and yet more austerity in public welfare spending and services.

* Michael Roberts worked in the City of London as an economist for over 40 years. He has closely observed the machinations of global capitalism from within the dragon’s den. At the same time, he was a political activist in the labour movement for decades. Since retiring, he has written several books. The Great Recession – a Marxist view (2009); The Long Depression (2016); Marx 200: a review of Marx’s economics (2018): and jointly with Guglielmo Carchedi as editors of World in Crisis (2018). He has published numerous papers in various academic economic journals and articles in leftist publications.

This article was previously published on his blowg here.